42 |

Investor Guide to Europe 2014

The Irish investment market is relatively small

and has historically been dominated by domestic

investors. The market has suffered in the wake of

the global financial crisis.

Following the swift action to create a Bad Bank in the form

of nAMA, the write down of loans and sharp re-pricing, the

Irish market is now witnessing a strong recovery, underpinned

by increased occupier demand, favourable policy measures

and improving economic sentiment. This is also supported by

growing interest from overseas investors, including the Uk,

USA and global opportunity funds.

The Irish market is dominated by Dublin, which represents

the bulk of investment activity, focussed on office, retail and

mixed-use schemes. The strength of transaction activity has

been characterised by a number of large sales and portfolio

sales, most notably, the Project Arc and Ulysses Portfolio. In

addition, there has been a noticeable increase in office market

investment activity.

The market has been dominated by private investors and

companies along with institutional investment. The listed

sector has been relatively small. However, legislation to create

REITs came into effect in 2013, since when Green REIT and

Hibernia REIT PlC have been launched to the market.

The supply of bank finance remains a concern, but has

improved in 2013. lending remains deal and borrower specific.

The extension of the capital gains tax window for investors

to December 2014 and low bank deposit rates should see

further entrants to the market as investors look for alternative

investments to inflation proof their capital.

Market sizing

Ireland

Europe

Invested stock*

(Total stock)

EUR 50bn

(EUR 70bn)

EUR 3,380bn

(EUR 8,150bn)

liquidity ratio*

(10y average)

2.6%

(2.0%)

4.0%

(4.5%)

2013 volumes

(10y average)

EUR 1.3bn

(EUR 1bn)

EUR 139bn

(EUR 135bn)

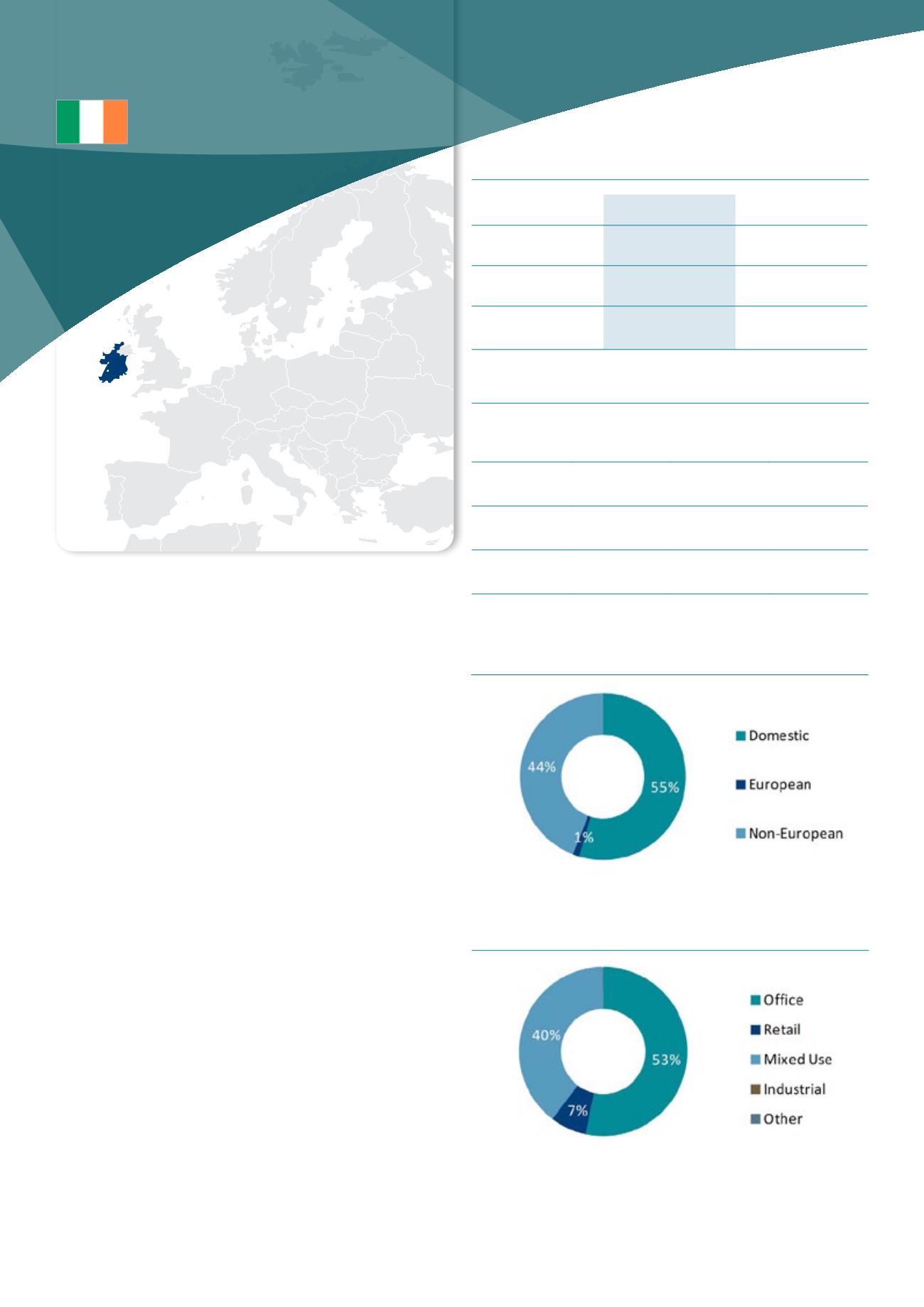

Investment activity by asset type, 2013

Source : DTZ Research

Investment activity by source of capital, 2013

Source : DTZ Research

Market pricing – Dublin (Q4 2013)

office

Retail

Industrial

Current Yield

5.75% 6.00% 8.50%

Min/Max

(10y)

4.00-7.50% 2.50-6.50% 5.50-9.25%

Yield

definition

net initial yield

Source : DTZ Research

IRELanD

* 2012 figures