108 / 132

108 / 132

Sweden

Sweden is the largest of the Nordic markets by

stock and the ninth largest market in Europe.

Although smaller than the UK, Sweden has had

the highest liquidity ratio over the past ten years

and is the second most liquid market globally.

Investment is not just focussed on the capital

Stockholm, but also across the country, which

provides more diversity for investors. The country has

a strong investor base, with many active institutions

and property companies. It also has an active listed

sector, although there are no REITs in Sweden.

Historically the market has seen strong levels of

domestic investment as well as overseas investors,

notably from neighbouring Norway and the UK. There

are also a number of funds active in sourcing capitals

from global investors.

Most investors focus on high-quality prime real

estate, especially within the office and retail

segments. Foreign investors concentrate mostly on

prime retail and logistics properties let on long-term

contracts. As there is a limited supply of property for

sale in the prime segment, an increasing number of

investors are tapping into the secondary segment.

Although impacted by the financial crisis, Sweden

has been seen as a relative safe haven, and market

activity recovered strongly from a low in 2009. Much

of this activity has been driven by domestic investors.

Swedish banks have also retained healthy balance

sheets and have not been as exposed to under-

performing loans. Debt is readily available, mostly

from traditional banks. Institutional lending remains

limited.

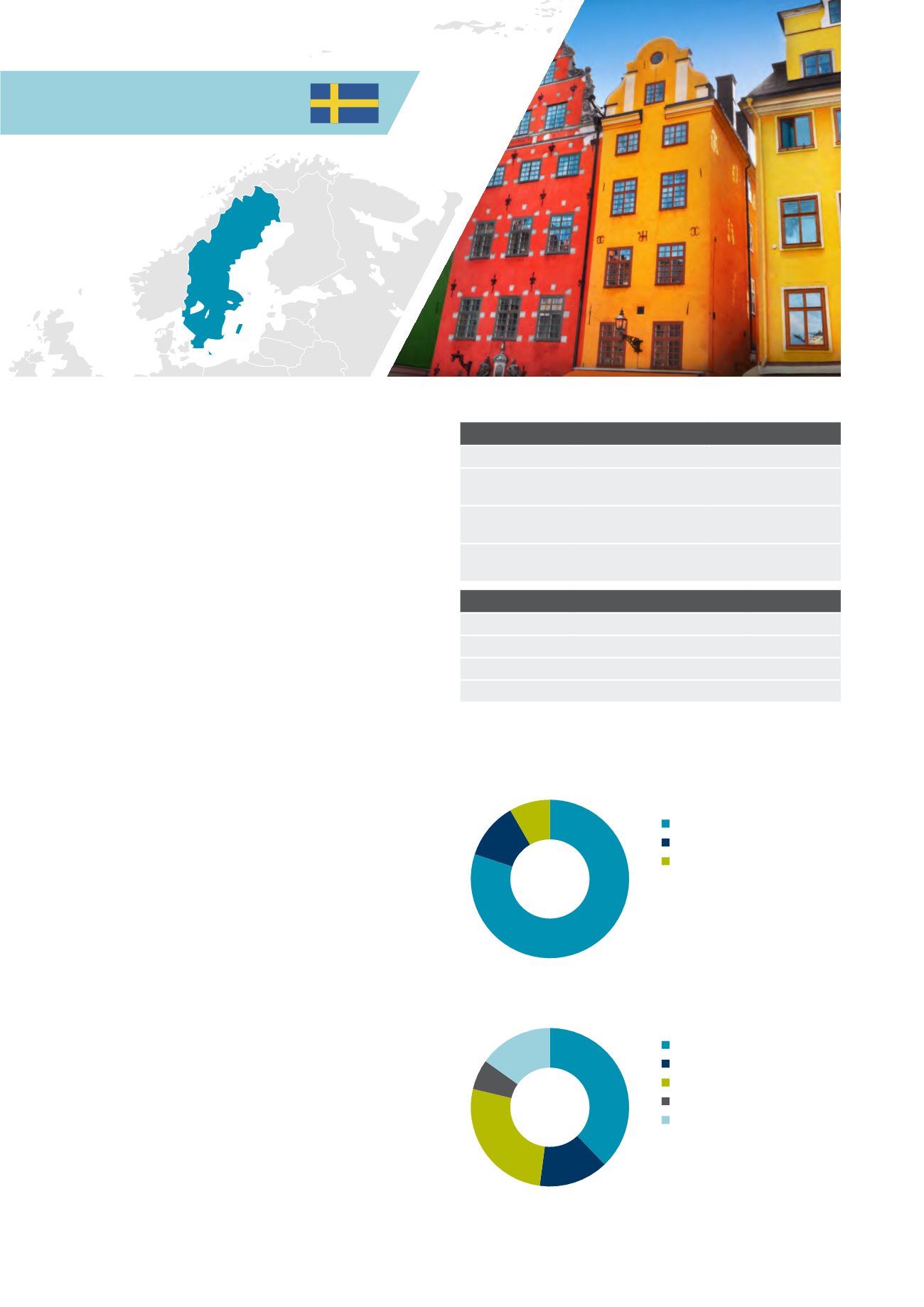

Market sizing

Sweden

Europe

Invested stock

(Total stock)

EUR 125bn

(EUR 160bn)

EUR 3,335bn

(EUR 8,201bn)

Liquidity ratio

(10y average)

9.4%

(8.8%)

5.6%

(4.6%)

2014 volumes

(10y average)

EUR 11.9bn

(EUR 9.2bn)

EUR 187bn

(EUR 142bn)

Market pricing – Stockholm (Q4 2014)

Office

Retail

Industrial

Current Yield

4.35% 4.25%

6.75%

Min/Max (10y)

4.25-5.75% 4.25-5.75% 5.75-7.75%

Yield definition

Net initial yield

Source: DTZ Research

Investment activity by source of capital, 2014

Investment activity by asset type, 2014

Source: DTZ Research

Source: DTZ Research

Domestic

Non-European

European

Office

Mixed Use

Retail

Industrial

Other

80%

8%

12%

38%

14%

27%

6%

15%

108 Investors Guide to Europe 2015